How Interest Rates Affect You

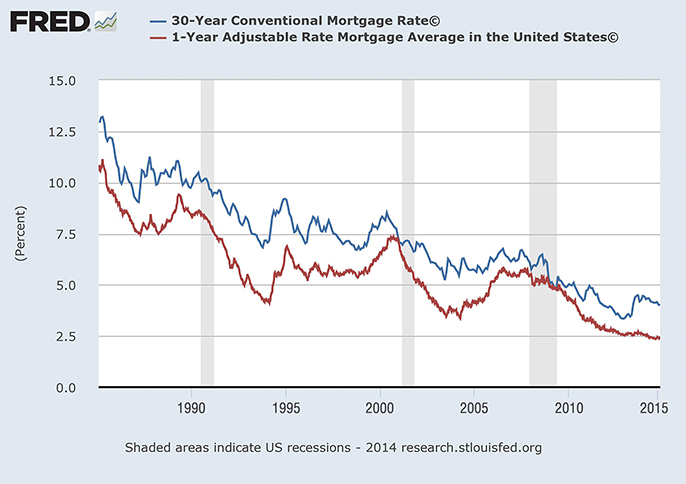

Recent years have seen mortgage interest rates at historic lows, creating an advantageous market for prospective homebuyers.† While interest rates aren’t the only deciding factor in making a home purchase, it’s important to understand how they can affect your buying power.

A lower interest rate can make a mortgage more affordable, not just in terms of monthly payments but also with the overall amount paid for the loan over time. The higher the interest rate, the more money the borrower will need to pay in interest over the term of the loan. For example, if you locked in an interest rate of 3.9% on a 30-year fixed-rate mortgage for a $500k home with 20% down, your monthly payment would be $1,887 (before taxes and insurance). At 4.9% interest, your monthly payment would increase by $236…but that adds up to an extra $84,960 over 30 years.

A change in the interest rate doesn’t necessarily translate to fluctuation in home prices, but they can affect the housing market. One big way interest rate changes affect the housing market is by affecting the amount you qualify for when applying for a loan. If there’s a 0.25% interest rate increase, for example, you might need 3% more income to qualify for the same mortgage.

{kind=link}